What happened to big work comp PPOs?

they thought they were in the network business.

15 years ago I predicted the big workers’ comp networks faced inevitable decline.

That day has come and gone, and with it the once-dominant position PPOs held in the work comp “cost containment” industry.

Today their effectiveness has declined in both absolute and relative terms…discounts below fee schedule/U&C have shrunk and other tools have supplanted PPOs in importance.

Why?

Two general reasons, both instructive for payers and service providers alike.

First, the Innovator’s Dilemma.

This more-than-a-theory holds that companies that are very successful in their fields keep improving their products, believing that what their customers want is more and better versions of the same. What these companies don’t do is think up new ways of meeting their customers’ needs; ways that are cheaper/faster/easier.

Instead, they work diligently on making their existing product a tiny bit better every year. And in the process, they don’t pay attention to what their customers actually need – the problem they are trying to solve.

The leading proponent of the theory, as well as the one who coined the term, is Clayton Christensen. Christensen’s research showed it is often entirely rational for existing companies to ignore new and disruptive innovations, because those new innovations don’t compare well with existing technologies or products. Even if a disruptive innovation is recognized, existing businesses are often reluctant to take advantage of it, since it would involve competing with their existing (and more profitable) technological approach.

Here’s an example from Christensen’s book, the Innovator’s Dilemma.

Back in the early- and mid-nineteen hundreds, the only way to dig big holes efficiently was to use a cable-actuated shovel driven by coal (initially) and later diesel. The cable shovel manufacturers got really good at making larger and larger shovels that could move yards and yards of dirt.

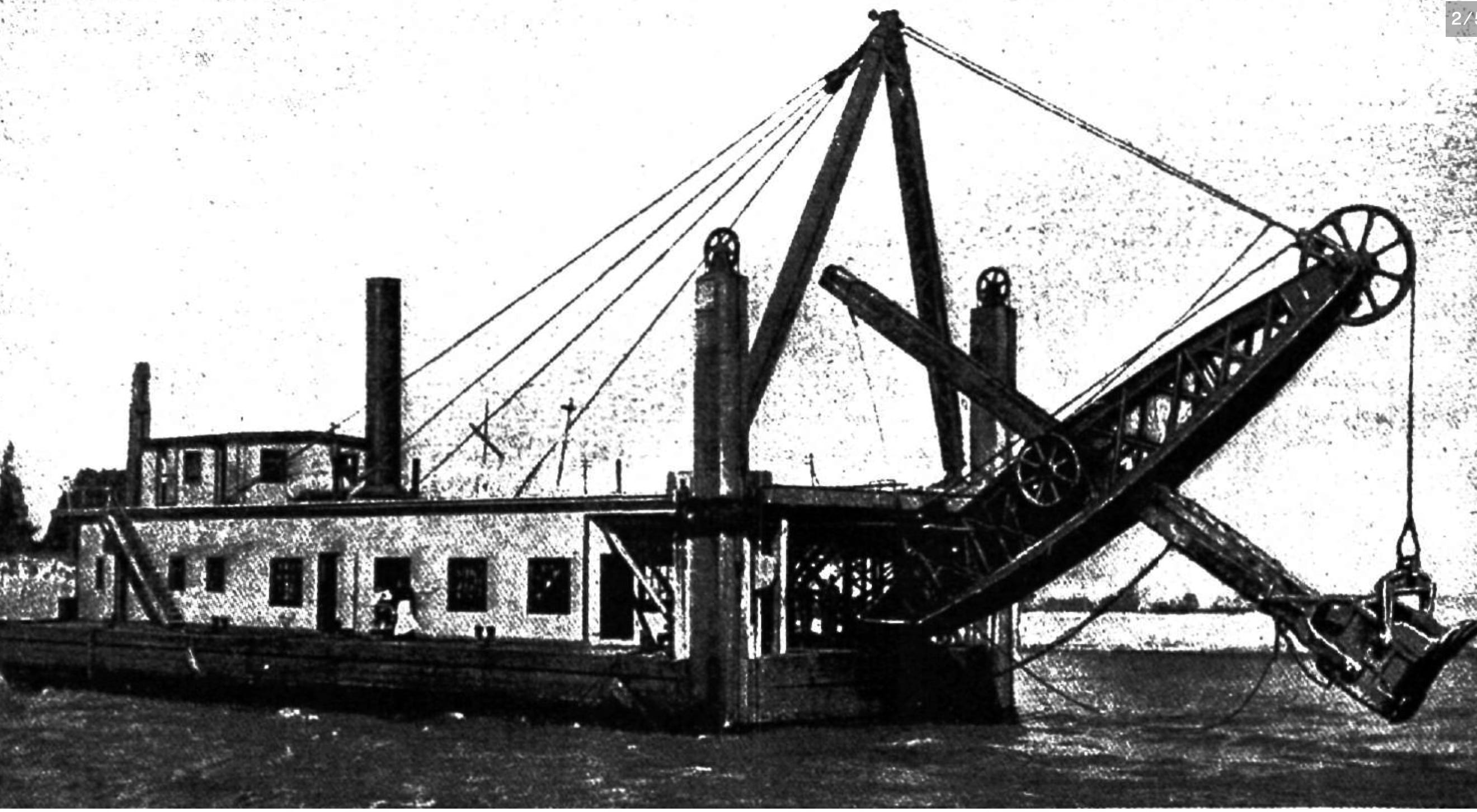

A Bucyrus Erie eye-powered shovel working at the Panama Canal

Meanwhile, other companies began developing hydraulically-driven shovels. At the start, these were small, puny affairs, barely able to move a third of a yard of dirt. Not surprisingly, the big cable shovel companies (e.g. Bucyrus Erie) laughed at the upstarts, knowing their customers were not interested in the toy version of their behemoth shovels.

But..lots of residential contractors and utilities could use the smaller shovels; their only alternative was hand-powered shovels. The new market entrants gradually improved their hydraulic shovels, until they could effectively move as much dirt as the biggest of the big boys. And do it more efficiently, with far fewer breakdowns, and much more safely.

Bucyrus Erie went bankrupt and eventually its remnants were acquired by Caterpillar.

Of all the big steam shovel companies in the business mid-century, only a small handful survived the onslaught of hydraulics, and the survivors did so by adopting the new technology. They found that the smaller end of their market was gradually taken over by the “toy” manufacturers, which then moved relentlessly up-market, until the only market left for Bucyrus et al was the hundred-yard plus strip mining shovel. Most of Bucyrus’ competitors went out of business, including the Marion Power Shovel Company. Marion employed over 2500 workers at its peak, when it made the largest steam shovels in the world to build the Panama Canal. When it was finally sold off in 2003, Marion had fewer than 300 employees.

{kind=link}

Back to our little world. The small, physician-only network never delivered big “savings” (in the form of discounts) and “penetration” (in the form of a really thick provider directory with most live and some dead docs listed therein) and therefore is not, in the view of the big network companies, something worth continued development. Sure they made attempts but these barely made a dent in the market.

I hasten to add their customers largely ignored or at best made half-hearted attempts to shift business models and adopt wide usage of the smaller networks…

What the big network companies missed is what their customers want to buy – not “savings” defined as discounts below fee schedule, but lower medical expenses and real outcomes.

After a decade-and-a-half of more and more networks delivering higher and higher medical expenses, big payers needed, and wanted, a different answer. Specialty networks and somewhat better, more sophisticated bill handling are now the most effective cost containment tools

But the big network companies have an even bigger problem, one that did not affect the cable shovel manufacturers. At the height of their business, there were no fewer than twenty companies making shovels, all working as hard as humanly possible to develop better and better cable shovels. They were innovating, all right, but their innovations were designed to make their core product better at moving more and more dirt.

What’s different in the comp network business is the almost complete lack of competition. Back in the day Coventry controlled upwards of 60% of the generalist network business, with the rest spread thinly between CorVel, Wellpoint, Horizon, Prime, and a few others. By all accounts, Coventry is not even bothering to improve their current product offering.

What does this mean for you?

It took the hydraulic shovel companies a good three decades to all but destroy the cable shovel business.

It took less than half that time for Coventry to lose its dominant position in work comp cost containment.

Next - the other driver of work comp PPOs’ shrinking importance.